The era of simplistic claims that art always increases in value has largely passed. Serious collectors and advisors now approach the market with a far more disciplined mindset. Art can play a role within a diversified portfolio, but it is not a replacement for equities, property, or traditional financial instruments. It is better understood as a passion asset, something that combines cultural significance with financial potential when approached intelligently.

This distinction matters because the art market behaves differently from most financial markets. Art does not produce income. It does not generate dividends or rental yields. Its value is determined by a complex interaction of cultural relevance, collector demand, institutional recognition, rarity, and historical pricing. Understanding those forces requires patience and expertise.

For many collectors, the attraction of art lies precisely in this combination. An artwork can hold personal meaning while also retaining financial value. Unlike purely financial assets, it can be lived with, studied, and experienced daily. This dual nature makes art one of the few investments that can deliver both intellectual reward and financial potential.

However, success in art investment rarely comes from speculation or short term thinking. It comes from understanding how the market actually works.

How The Art Market Actually Works in 2026

Historically the art market has been opaque. Prices were often private, information was fragmented, and access to reliable market data was limited to a small network of dealers and auction specialists. Collectors relied heavily on personal relationships and institutional knowledge to navigate the market.

Over the past decade that landscape has begun to change. Digital platforms, improved data analysis, and increased transparency around auction results have made it easier for collectors to observe pricing trends and demand signals. While the art market remains far from perfectly transparent, certain segments now offer far greater clarity than they did even ten years ago.

Investing in Prints & Editions

One of the most important developments has been the growth and visibility of the secondary market for modern and contemporary prints and editions.

Unlike unique paintings or sculptures that may sell only once every decade or two, prints exist in editions. Multiple examples of the same work may appear on the market over time. Each sale contributes another data point, gradually building a record of comparable transactions.

This accumulation of comparables allows collectors to track pricing behaviour in ways that are much closer to traditional asset markets. When a work from a particular edition sells repeatedly across auctions and private sales, collectors can observe patterns of demand and price development.

In this sense, prints function as one of the most data rich segments of the art market.

At MyArtBroker we have spent more than 15 years tracking this space across a core group of artists whose print markets demonstrate consistent liquidity and global demand. These include Andy Warhol, Banksy, David Hockney, Roy Lichtenstein, Keith Haring, Bridget Riley, Yayoi Kusama, and Damien Hirst.

Each of these artists occupies an important position within modern and contemporary art history. Their works are held by major museums and institutions around the world. Their imagery is widely recognised and their collector bases span multiple generations and continents.

The combination of cultural relevance and measurable market activity creates an environment where collectors can approach acquisitions with greater confidence.

This does not mean art becomes a purely financial instrument. Taste, scholarship, and historical understanding still matter enormously. The difference is that collectors now have access to far more information when making decisions.

Technology can surface signals such as auction results, comparable sales, and demand indicators. Yet interpreting those signals still requires the expertise of specialists who understand the nuances of artists, editions, and market cycles.

In other words, data can inform decisions, but it cannot replace judgement.

Understanding this balance is essential for anyone considering art as part of a broader investment strategy.

Q: What is the alternative asset class and how does art fit within that category?

A: An alternative asset falls outside traditional classes such as stocks, bonds and cash. They appeal as a secondary investment in addition to the former, as they can strengthen and diversify traditional portfolios by seeking returns independent from equity and bond markets. Art is classified as an alternative asset because its market is not correlated with other assets.

To learn more about the concept of prints as an investable asset, watch our panel: Prints as a Portfolio.

Is Art a Good Investment?

Before exploring how to invest in art, it is worth asking a more fundamental question. Should art be considered an investment at all?

In financial terms art is classified as an alternative asset. Alternative assets sit outside traditional financial instruments such as stocks, bonds, and cash. Investors often allocate to alternatives in order to diversify portfolios and reduce correlation with financial markets.

Art fits within this category because its value is not directly linked to stock market performance or interest rates. However, art differs from most alternative assets in one crucial respect. It does not produce income.

The return on an artwork depends entirely on its resale value. This means that collectors must consider not only what they buy but also whether there will be demand for the work in the future.

For this reason the most experienced collectors rarely approach art purely as a financial trade. Instead they combine cultural curiosity with financial discipline. They build collections around artists and works they believe in intellectually while also considering market dynamics.

There is a useful comparison with the property market. When purchasing real estate, investors rarely make decisions based solely on aesthetic preference. They research comparable sales in the neighbourhood, examine historical price trends, and evaluate long term desirability.

Art works in much the same way. When collectors can observe comparable sales and understand how an artist’s market behaves over time, the process becomes far more structured.

This is where the secondary market plays a crucial role.

The primary market involves artworks being sold for the first time, usually through galleries representing living artists. Prices are typically set by galleries and may reflect curatorial momentum, institutional exhibitions, or demand from a specific collector base.

While the primary market can be an exciting place to discover new artists, it is also one of the most difficult markets to analyse from an investment perspective. Without historical sales records there are few comparables on which to base pricing decisions.

The secondary market operates differently. It involves artworks that have already been sold and are now trading again through auction houses, dealers, and private sales. Each resale creates a record that collectors can examine.

Over time these transactions build a picture of how an artwork or artist performs within the market.

Few people understand the financial side of this process better than Philip Hoffman, founder of The Fine Art Group. Before entering the art world Hoffman trained as a chartered accountant at KPMG and later became Chief Financial Officer of Christie’s during a period when the auction house was undergoing significant financial restructuring.

After leaving Christie’s he went on to establish one of the earliest large scale art investment funds, raising hundreds of millions of dollars from institutional investors and building a business that now advises collectors and institutions worldwide.

During a conversation recently about the realities of art funds he explained that many investors underestimate the discipline required. People assume art funds are easy. They are not. You have to buy extremely well, understand the market in extraordinary detail, and manage liquidity very carefully. Otherwise it is very difficult to deliver returns.

His observation reflects a broader truth about art markets. Successful collecting rarely comes from speculation. It comes from understanding supply, recognising demand, and buying works that other collectors will also want in the future.

In practice this often leads collectors toward segments of the market where demand is already well established. The secondary market for prints is one of the clearest examples of this.

Because prints exist in editions, collectors can observe how individual works perform across multiple sales over time. This accumulation of pricing data allows buyers to understand market behaviour with greater clarity than in markets for unique works.

For many collectors this transparency is what makes prints such an attractive entry point into the art market.

How to Invest in Art: Key Strategies

There are several different ways to gain exposure to the art market. Some collectors purchase artworks outright and build personal collections. Others participate through managed funds, fractional ownership platforms, or newer digital formats.

Each approach carries its own advantages and risks. The most important factor is understanding the structure of the market you are entering.

Unlike financial markets, the art world does not operate through a single exchange. It is fragmented across galleries, auction houses, dealers, brokers, and private networks. Prices can vary depending on where and how a work is sold.

Because of this fragmentation, intelligent collectors tend to focus on areas where pricing and demand are easiest to observe.

In practice this usually means starting with the secondary market.

1. 100% Art Ownership

The most traditional way to invest in art is also the simplest. A collector purchases an artwork outright and becomes its sole owner. Full ownership allows collectors to live with the artwork, loan it to exhibitions, or eventually sell it when market conditions are favourable. It also provides complete control over acquisition and sale decisions.

Collectors can acquire works through galleries, auction houses, private dealers, or brokerage platforms. Each channel offers different advantages depending on the type of work and the collector’s objectives. However the key decision collectors face is not only what to buy but where within the market to buy it.

Buying on the Primary vs. Secondary Market

The art market is typically divided into two major segments.

The primary market involves artworks being sold for the first time, usually through galleries representing living artists. Prices are set by galleries and may reflect curatorial reputation, institutional attention, or demand among collectors.

The secondary market involves artworks that have previously been sold and are now trading again. These transactions take place through auctions, dealers, and private sales.

From an investment perspective the secondary market often provides greater clarity because historical sales records exist.

Repeated transactions create comparable pricing data. Collectors can observe how works have traded over time and how demand behaves across different market cycles.

This is particularly true in the prints market.

Because prints exist in multiples, individual works from the same edition may appear on the market many times over decades. Each transaction adds to the record of comparable sales.

Over time this creates a pricing framework that collectors can analyse.

‘Blue Chip’ Print Markets

Certain Modern and Contemporary artists have developed especially strong secondary markets for prints and editions.

Andy Warhol

Warhol’s prints form the backbone of the modern print market. Series such as Marilyn, Flowers, and Campbell’s Soup Cans have traded consistently for decades and remain among the most recognised images in contemporary art.

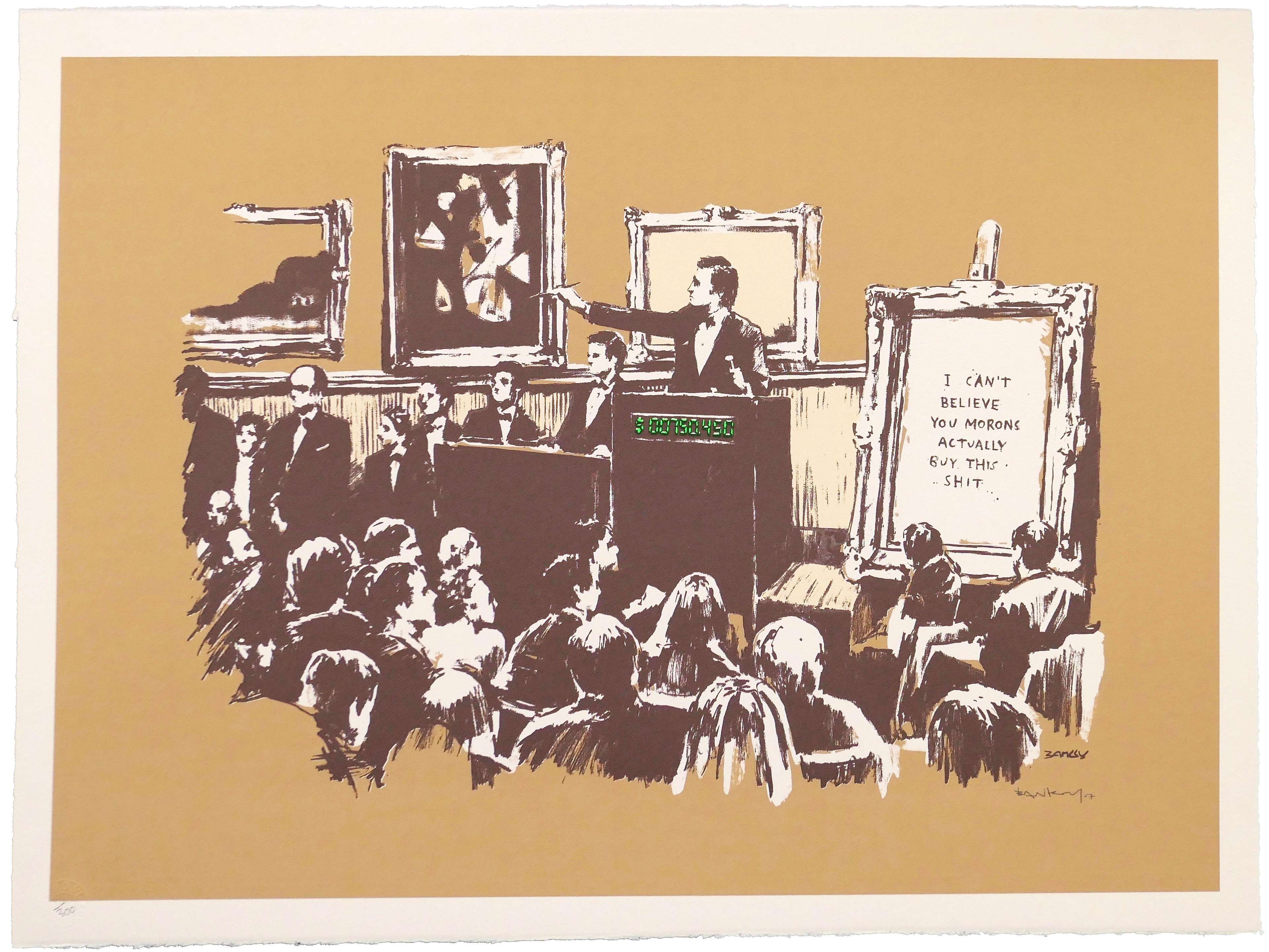

Banksy

Banksy’s editioned works have developed one of the most liquid secondary markets in contemporary art. Prints such as Girl With Balloon and Choose Your Weapon are widely recognised and frequently traded across auctions and private sales.

David Hockney

Hockney’s printmaking career spans more than sixty years. His works range from early etchings to the celebrated Arrival of Spring iPad drawings, each supported by strong institutional recognition.

Roy Lichtenstein

Lichtenstein’s Pop Art prints remain among the most stable segments of the post war market. Their graphic clarity and art historical significance continue to attract collectors worldwide.

Keith Haring

Haring’s prints combine cultural relevance with limited edition sizes. Works from the Pop Shop series remain highly sought after among collectors.

Bridget Riley

Riley’s optical prints are supported by decades of museum recognition and scholarly attention, creating a stable and respected secondary market.

Yayoi Kusama

Kusama’s global popularity and distinctive visual language have helped establish a strong market for her prints.

These markets share an important characteristic. They are well documented and actively traded, allowing collectors to observe pricing trends over time.

2. Digital Art

Digital art has become one of the most visible developments in the art market over the past decade.

The emergence of NFTs in the early 2020s briefly transformed digital artworks into a major speculative asset class. The sale of Beeple’s Everydays The First 5000 Days for $69 million at Christie’s captured global attention and introduced a new generation of collectors to the concept of blockchain based ownership.

NFT technology allows digital files to be linked to unique tokens recorded on a blockchain. These tokens provide a verifiable record of ownership and transaction history.

In theory this offered a solution to one of the traditional challenges of digital media. Digital files can be copied infinitely, making it difficult to establish scarcity. NFTs attempted to create scarcity through cryptographic ownership.

However the rapid rise of the NFT market was followed by significant volatility. Many prices were driven as much by speculation as by long term collecting behaviour. When cryptocurrency markets cooled, demand for many NFTs declined sharply.

Digital art continues to evolve as a medium, particularly through generative systems and artificial intelligence. Auction houses and galleries continue to experiment with these forms. But compared with more established segments of the art market, digital art remains relatively young. It lacks the decades of comparable sales data and institutional history that support more mature markets.

For collectors comfortable with higher levels of risk the digital art market can be an interesting space to explore. However from a purely investment perspective it remains less predictable than segments such as the secondary prints market.

3. Art Investment Funds

Art investment funds attempt to treat artworks as a structured financial asset.

Instead of purchasing individual works, investors contribute capital to a managed portfolio of artworks. Fund managers then acquire works on behalf of investors and eventually sell them to generate returns. In theory this model offers diversification and professional expertise. In practice art funds face several structural challenges. Liquidity is one of the most significant. Selling an artwork can take months or even years depending on market conditions and buyer demand. Fund managers must therefore carefully manage acquisition and exit strategies.

Another challenge lies in valuation. Unlike financial securities, artworks do not trade continuously. Pricing often relies on comparable sales and specialist judgement. Despite these complexities art funds have contributed to a broader conversation about art and wealth management. Increasingly wealth advisors consider art and collectibles as a potential component of diversified portfolios, although usually as a relatively small allocation.

For individual collectors the lessons of art funds are less about the funds themselves and more about the discipline they require. Successful art investment depends on buying well, understanding the market, and exercising patience.

4. Fractional Shares

Fractional ownership represents a newer approach to art investment. Instead of purchasing an artwork outright, investors buy shares in a work. Multiple individuals may therefore hold partial ownership of a single piece.

Some platforms use blockchain technology to record these shares while others operate through traditional financial structures. The appeal lies in accessibility. Investors can gain exposure to artworks that might otherwise be financially unattainable.

However, fractional ownership introduces new considerations. Investors often have limited control over when the artwork is sold. Decisions about timing are typically made by the managing platform. Because the sector remains relatively new there is also limited long term performance data.

For collectors interested primarily in the cultural experience of owning art, fractional ownership may feel somewhat removed from traditional collecting. For others it may offer a way to participate financially in high value artworks.

The art market offers many different ways to participate. Collectors can purchase artworks outright, invest through funds, explore digital formats, or experiment with fractional ownership.

Yet despite the emergence of new models the fundamental principles of art investment remain remarkably consistent.

Successful collectors tend to focus on markets where demand is visible, pricing is comparable, and cultural significance is well established.

This is one reason the secondary market for blue chip prints and editions continues to play such an important role. Artists such as Warhol, Banksy, Hockney, Lichtenstein, Haring, Riley, and Kusama have developed global collector bases and deep secondary markets. Their works trade regularly across auctions and private sales, generating the comparable data that allows collectors to analyse value.

In an art market that has historically been opaque this transparency is unusual. It does not remove risk. Art prices still fluctuate and tastes evolve. But when collectors combine historical pricing data with specialist expertise the market becomes far easier to navigate.

As technology continues to reshape the art world the most effective approach will likely remain the same balance between data and expertise.

For collectors willing to approach the market with patience, curiosity, and discipline, art remains one of the few assets capable of delivering both cultural significance and long term financial potential.