Key Takeaways

- Prints and editions can be strong long-term investments when they sit within active secondary markets with repeat sales, visible pricing, and sustained collector demand.

- Blue chip prints by Warhol, Hockney, Banksy, Haring, Lichtenstein, Riley, Hirst, Basquiat, and Kusama continue to anchor the most established segments of the market.

- Liquidity matters as much as scarcity: the best limited edition prints are not only rare, but consistently tradable at fair market value.

- Edition size, signature, condition, provenance, and series-level demand all shape the value of a limited edition print.

- Buying limited edition prints online requires due diligence, including checking authenticity, edition structure, and real resale comparables rather than relying on asking prices.

- Series and portfolios often behave like micro-markets, meaning collectors should assess individual collections such as Warhol’s Marilyns or Hockney’s Arrival Of Spring rather than artists in general.

- The print market in 2026 is more disciplined than in 2021, with demand concentrating around recognisable imagery, strong market history, and quality works priced in line with current conditions.

- Private sales are increasingly important in the mid-tier market, particularly for prints and editions between roughly £20,000 and £250,000.

At a time when the broader market has become more selective, that level of transparency matters. According to the Art Basel UBS Art Market Report, the global art market fell by 12% in value in 2024 to an estimated $57.5 billion, yet transaction volumes still rose by 3%, a sign that activity has not disappeared so much as shifted toward segments where buyers can still find price evidence and act with conviction. In their latest 2026 report, global sales recovered to an estimated $59.6 billion in 2025, with public auction sales rising 9% year on year, reinforcing the sense that buyers remain active where quality, pricing, and demand align.

That is why more collectors are asking not simply whether prints are “worth buying”, but which prints make sense to buy now, under what market conditions, and with what expectations around resale, value, and long-term collectability. In the blue chip editions market, the strongest opportunities tend to sit where cultural relevance, repeat sales activity, disciplined supply, and established demand meet. That is the space MyArtBroker specialises in: the secondary market for modern and contemporary prints and editions, supported by live market data, private sales intelligence, and specialist guidance designed to bring more control to buying, selling, and collection-building.

Why prints and editions have become a serious collecting category

The biggest misconception about prints is that they are simply the “entry point” to real collecting. In reality, original prints and editioned works can be among the most functional assets in the art market. In a limited edition, supply is fixed from the outset. Collectors know how many impressions exist, whether a work is signed, whether there are proof variants, and, in many cases, how often that exact work has traded publicly before. That visibility gives prints a degree of market memory that unique works often lack.

This is particularly important in a more disciplined market. The post-pandemic surge of 2021 created pricing distortions across parts of the art world, but the correction that followed has sharpened buyer behaviour rather than extinguished it. Collectors are now more selective, more comparative, and less willing to pay for narrative without evidence. In prints and editions, that has favoured works with repeat sales histories, recognisable iconography, and established buyer depth. Prints should not be seen as a compromise, but as one of the most sophisticated segments of the market because they allow a collector to evaluate supply, demand, and pricing behaviour with unusual clarity. That position is strengthened by the wider market data: in 2024 and 2025, the lower and middle price tiers showed greater resilience than the thinning top end of the global market.

Are limited edition prints a good investment in 2026?

They can be, but only when approached correctly.

A limited edition print is not valuable simply because it is limited. Nor does a signature automatically make a work “investment grade”. Value in the secondary print market is usually shaped by a combination of factors: the artist’s market strength, the desirability of the image or series, edition size, condition, provenance, frequency of resale, and the depth of the buyer pool for that exact work.

In other words, the best blue chip prints are not just scarce. They are also tradable.

That distinction is especially important in 2026. Serious collectors are increasingly looking for works that combine cultural significance with measurable resale behaviour. In practice, that means demand is concentrating around historically established names and internally coherent micro-markets: Andy Warhol’s Cowboys & Indians, Marilyns, and Endangered Species; David Hockney’s The Arrival Of Spring, Moving Focus, and Swimming Pools; Roy Lichtenstein’s Nudes; Banksy’s Girl With Balloon and Choose Your Weapon; and selected portfolios by Keith Haring, Bridget Riley, Damien Hirst, Jean-Michel Basquiat, and Yayoi Kusama. The most resilient print markets are built not around artist names in the abstract, but around repeatable series where liquidity, comparables, and collector attention remain concentrated.

You can learn more about the Top 10 Most Investable Prints Series & Collections here.

What makes a print “investable” in the secondary art market?

1. A strong artist market

Blue chip artists are blue chip because their markets have depth. They benefit from sustained institutional support, broad collector recognition, and repeat sales over time. In the current market, some of those markets include: Warhol, Banksy, Hockney, Haring, Lichtenstein, Riley, Hirst, Basquiat, and Kusama.

2. A series with internal structure

Some print markets are too broad to assess in general terms. The more useful question is often whether a specific series behaves well. Does it trade regularly? Are there clear tiers between main editions and proofs? Are complete sets or matching-number groups especially desirable? Are certain motifs or colourways structurally stronger than others?

3. Repeat sales and price evidence

A print with one exceptional result is not necessarily a strong market. A print that trades repeatedly, within a recognisable range, is often a more reliable indicator of demand. Liquidity is not hype. It is repeatability.

4. Condition and edition integrity

Two impressions of the same work can trade very differently. Margins, handling, paper quality, restoration history, framing, and storage all affect value. So do missing documents, weak provenance, or confusion around proof status and edition structure.

5. Timing and channel

A good print can still be poorly bought. Timing matters, and so does the route to market. Auction can provide visibility, but private sales are increasingly important in the mid-market, where careful buyer matching and controlled pricing often produce better outcomes than public theatre. Art Basel & UBS’s latest reporting shows that public auction sales rose in 2025, but auction house private sales declined, underlining that market structure is still shifting and that buyers need a more nuanced understanding of where liquidity is actually happening.

Limited edition prints vs originals: which offers more control?

Original artworks can carry extraordinary upside, but they also tend to come with more opacity. A unique work may be culturally significant and rare, but rarity alone does not guarantee ease of resale. Pricing can be highly context-dependent, demand may be narrow, and comparables are often imperfect.

Prints and editions occupy a different position. Because they are editioned, they generate more points of comparison over time. Collectors can often see how the same image has behaved across multiple transactions, how proof variants sit against the main edition, and whether the market is widening or narrowing. That makes prints particularly attractive to collectors who want to buy with value in mind without losing sight of visual and historical quality.

For that reason, many serious collections now use prints as a strategic layer rather than a starter category. They provide access to museum-grade artists, but with more measurable pricing and, in many cases, stronger optionality on exit.

Where demand is concentrating in the print market now

The current market is rewarding quality, recognisability, and disciplined supply. Recent signals from London’s March 2026 sales reflect that clearly. Works by Banksy, Warhol, Hockney, and Lichtenstein either exceeded estimates or held firmly within them, with particular strength around familiar imagery and historically significant works. That pattern aligns with the broader market backdrop: confidence has returned selectively, not indiscriminately. Buyers are still spending, but with much tighter attention to what has already demonstrated staying power.

Andy Warhol prints

Warhol remains one of the deepest and most internationally traded print markets. Demand continues to concentrate around portfolios with clear internal hierarchies and recognisable imagery, including Marilyn Monroe, Endangered Species, Cowboys & Indians, Flowers, and selected late works. Warhol’s market also benefits from breadth: complete sets, main editions, APs, and more unusual proof categories create multiple collecting levels rather than a single narrow pricing band.

David Hockney prints

Hockney’s market continues to intensify under significant institutional reinforcement. The Serpentine is currently showing David Hockney: A Year in Normandie and Some Other Thoughts about Painting from 12 March to 23 August 2026, while recent years have also included Drawing from Life at the National Portrait Gallery and the major David Hockney 25 exhibition at Fondation Louis Vuitton. That concentration of institutional visibility matters because it supports collector confidence across both historic and digital chapters of his practice. In print terms, The Arrival Of Spring remains one of the clearest examples of a series whose internal hierarchy has shifted upward, while Moving Focus and the Swimming Pools group continue to offer mature, structurally coherent demand.

Roy Lichtenstein prints

Lichtenstein’s print market has entered a more concentrated upper tier, particularly around the Nudes and other rare formats. The Whitney has a major Lichtenstein retrospective in planning for 2026, while the Foundation’s current exhibition listings underline the artist’s centennial-level visibility. As with Hockney, institutional reinforcement has coincided with stronger pricing at the top end of the print market.

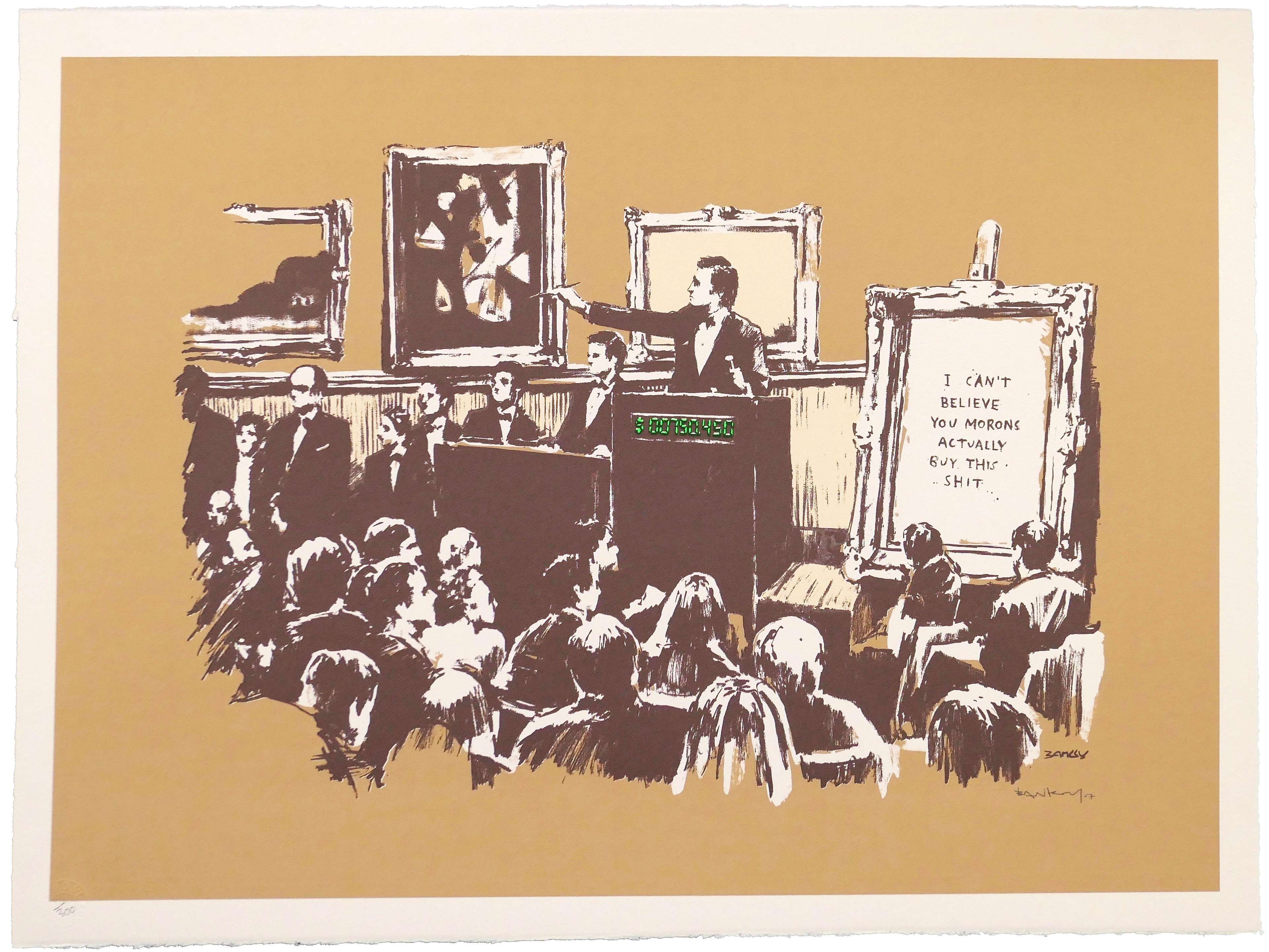

Banksy prints

Banksy remains one of the most liquid contemporary print markets, but he is also a reminder that liquidity does not eliminate cycles. Works such as Girl With Balloon and Choose Your Weapon still benefit from strong global recognition and deep comparables, yet buyers are notably more disciplined than they were at the 2021 peak. That does not weaken the market; it makes it more legible.

How to buy limited edition prints online without overpaying

Buying online is no longer unusual in the print market. The more relevant question is how to buy online properly.

Start with the exact work, not a broad category. Confirm the title, year, edition size, medium, and whether the impression is from the main edition or a proof category such as AP, PP, TP, or HC. Check whether the print is signed and whether any certificate, invoice, or publisher documentation is available. Then look beyond the seller’s asking price. Asking prices are not the market. They are invitations. What matters is where that exact work has actually traded, how recently, and under what conditions.

Condition is equally important. A print that looks clean in a JPEG may have trimmed margins, surface rubbing, acid burn, restoration, or framing issues that materially affect value. Buyers should also be cautious around works offered “sold framed” without full examination. In higher-value markets, especially Banksy, authentication is non-negotiable.

This is where specialist-led platforms have a meaningful advantage over general marketplaces. MyArtBroker’s model is built around the secondary market for prints and editions, with data-backed valuations, deep specialist input, and tools designed specifically for this category rather than the art market at large.

Why liquidity matters more than headline prices

One of the most misunderstood ideas in art collecting is liquidity. It does not mean that a work is famous, nor that it has once made a high price. It means that the work can sell again, at a fair level, within a market that has enough comparables and enough buyer depth to support confidence.

This is why prints and editions often play such an important role in serious collections. They can offer something many unique works cannot: repeat-traded evidence. In a selective market, that evidence is increasingly valuable. The best-performing collectors in 2026 are not necessarily buying the loudest works. They are buying the works that make sense structurally.

Final thoughts: should you invest in prints and editions in 2026?

For the right collector, yes.

But the real opportunity is not in buying “prints” as a category. It is in understanding which prints have the strongest market structure behind them. In 2026, the best blue chip print markets are defined by recognisable imagery, established artist demand, coherent series-level behaviour, disciplined supply, and repeat sales activity. That is why prints and editions continue to attract serious attention even in a more selective market. They offer access, certainly, but they also offer something rarer in the art world: a greater degree of control.